On Tuesday 16 April Treasury finally released the long awaiting rules for the $130bn JobKeeper program. The same day the ATO released some practical detail on how the administration of the program will work.

We have included some details that had previously been unclear below. If you have any questions about JobKeeper please contact your advisor or send us an enquiry at [email protected].

- How do we test Turnover drop?

April Eligibility it based on a 30% drop comparing any of the following periods (your choice):- Actual March 20 to March 19

- Projected April 20 to April 19

- Projected June Qtr 20 to June Qtr 19

- How to calculate Turnover?

They have defined this as “GST turnover”.

UPDATE: Despite what the legislation says, the ATO have advised that if you prepare your BAS on a cash basis, they will accept a cash basis calculation – though you still have the option to calculate on an accruals basis. A business that reports on an accruals basis MUST report on an accruals basis.

- What if my projection is wrong?

Provided your projection was prepared on a “reasonable basis” (and you would need evidence to justify your projection) – if it turns out that it was wrong – there is no penalty or clawback. But ATO could argue your projection wasn’t reasonable.

Example. You have a cafe and you have shut your doors at the end of April. You therefore project that your June Quarter income is down 30%. If the government announces the social distancing restrictions are lifted at the end of May, and the business has an exceptional June trading so you are only down 10% for the quarter vs the June 19 quarter – you’d have a pretty good argument that your projection was reasonable at the time you made it because you didn’t know the lock down would be lifted.

- Do you have to maintain the 30% drop over the JobKeeper period?

No – once you qualify for the scheme, you are eligible for the remaining duration (up to 6 months). You will still need to report monthly to the ATO both your actual (prior month) and projected (next month) turnover.

- But if I just stop invoicing for April won’t I become eligible?

Do not do this!!! Anti-avoidance measures have been introduce to detect and stop this happening. If you have been involved in a “scheme” to make your business eligible for the program – they will claw the funds back and charge interest and other penalties. They are on the look out – Just don’t do it!!!

- When can I register?

You can currently only register your interest for JobKeeper – Registration opens 20/04 – you can enrol directly through the business portal, or we can help.

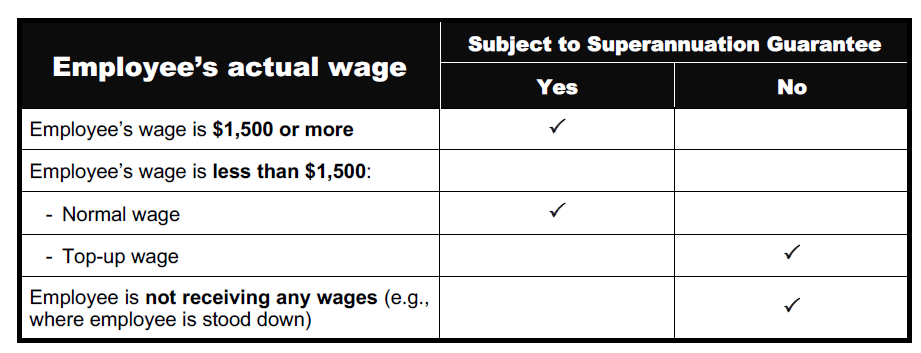

- If I have stood my employees down and pay them the $1500 – do I need to pay super on it?

No.

- Are JobKeeper payments taxable?

Yes – Taxable to the employer who receives them and taxable to the employee.

- Do I have to deduct PAYGW from employee payments?

Yes

- If I meet the turnover test for April, but I haven’t paid my employees the $1500 because they’re stood down without pay or earn less than that normally… am I still eligible?

Only if you make catch up payments to the employees.

Normally the payment must be made by the end of the relevant fortnight – but the ATO has allowed a concession for the first two fortnights (April) as long at the payments are made by the end of April you can receive the JobKeeper payment.

- This all seems really complicated….

Tell me about it!

There are many more questions we will update this blog with them as they come out.