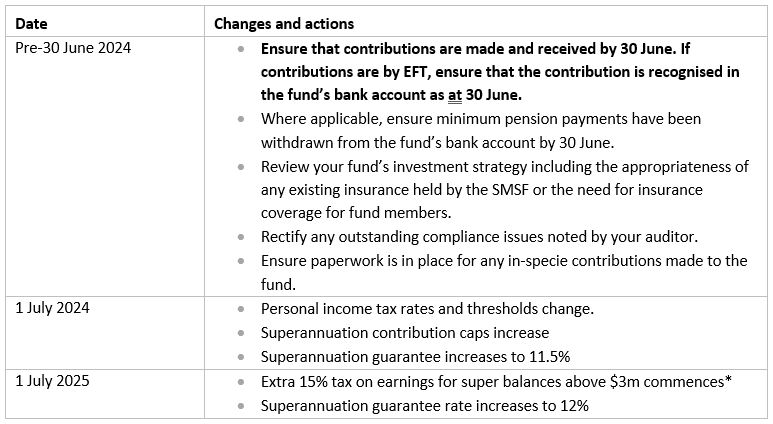

Our 2024 EOFY update and actions for Self Managed Superannuation Funds will give you an overview of tax changes and some actions you can take to reduce your tax exposure and minimise risk of an audit.

Self Managed Superannuation Funds continue to be a focus for the Government and the regulators, and a number of changes are being enforced to tighten control over how SMSFs operate.

We want to help you achieve the best result for you and your SMSF. If there is any additional information we can provide, or if we can assist you with your individual situation, please contact us today.

What’s New:

- In Brief

- Personal Income Tax Thresholds from 1 July 2024

- Superannuation Contribution Cap Increase

- Superannuation Guarantee increases to 11.5%

- 30% Tax on Super earnings for balances above $3m

- What’s not changing

- Areas of ATO concern

- Fund Housekeeping

- What we need from you – a general list of what to prepare before your next meeting with us

We want to help you achieve the best result. If there is any additional assistance we can provide, or if you would like us to review your situation, please call us on 02 8378 2421.

In Brief

*Pending legislation. Not yet law.

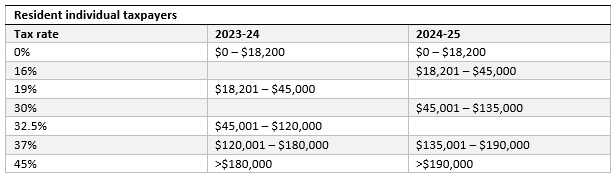

Personal Income Tax Thresholds from 1 July 2024

The personal income tax rates and thresholds will change from 1 July 2024.

If you are likely to have a personal income tax debt this financial year, and building your superannuation is a strategy you are pursuing, consider making a deductible contribution to superannuation.

Deductible contributions

If your total superannuation balance allows it, and you have not used your $27,500 concessional contribution cap, you could make a one-off deductible contribution before the end of the financial year and take the higher tax deduction. The cap includes superannuation guarantee paid by your employer, amounts you have salary sacrificed into super, and any amounts you have contributed personally that will be claimed as a tax deduction.

To make a deductible contribution to your SMSF, you need to be aged under 75, lodge a notice of intent to claim a deduction in the approved form with your SMSF and get an acknowledgement from the fund before you lodge your tax return (yes, even if you are giving the paperwork to yourself in your role as trustee). For those aged between 67 and 75, you can only claim a deduction on a personal contribution to super if you meet the work test (i.e., work at least 40 hours during a consecutive 30-day period in the income year, although some special exemptions might apply).

Be aware that any concessional contributions you make are included in the threshold for the high income earner, Division 293 tax. If the total of your assessable income and your concessional contributions is above the threshold ($250,000 for 2023-24), then 15% tax is charged on the excess over the threshold or the taxable super contributions, whichever is less. If you are likely to be close to the threshold, check that any concessional contributions you are planning to make have the intended impact.

Catch-up concessional contributions

If your superannuation balance on 30 June 2023 was below $500,000, you might be able to access any unused concessional cap amounts from the last five years in 2023-24 as a personal contribution. For example, if you were $8,000 under the cap in each of the last 5 years, you could contribute an additional $40,000 and take the tax deduction in this financial year at the higher personal tax rate.

Tax offset for spousal contribution

If your spouse’s assessable income is less than $37,000 and you both meet the eligibility criteria, you could contribute to their superannuation and claim a $540 tax offset.

Superannuation Contribution Cap Increase

From 1 July 2024, the amount you can contribute to superannuation will increase from $27,500 to $30,000 for concessional super contributions and from $110,000 to $120,000 for non-concessional contributions.

The contribution caps are indexed to wages growth based on the prior December quarter’s average weekly ordinary times earnings (AWOTE). Growth in wages was large enough to trigger the first increase in the contribution caps in 3 years.

Other areas impacted by indexation include:

- The Government super co-contribution – Income threshold

- The super guarantee maximum contribution base (the limit for compulsory super guarantee payments)

- The tax-free thresholds for redundancy payments

- The CGT contribution cap (amount that can be contributed to super following the sale of eligible business assets)

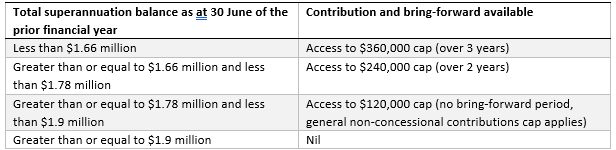

Utilising the bring forward rule

The bring forward rule enables you to bring forward up to 2 years’ worth of future non-concessional contributions into the year you make the contribution – this is assuming your total superannuation balance enables you to make the contribution and you are under age 75.

After 1 July 2024, the maximum that can be contributed under this rule will be $360,000.

Contribution and bring-forward available to members under 75 from 1 July 2024

If you trigger the bring forward rules in 2023-24, you will not get the benefit of the 1 July 2024 cap increase. Therefore, if you are contemplating using the bring forward rule to maximise your superannuation, if you can, wait until after 1 July 2024 and utilise the higher non-concessional contribution cap.

Superannuation Guarantee increases to 11.5%

The Superannuation Guarantee (SG) rate will rise from 11% to 11.5% on 1 July 2024 and will continue with a final increase to 12% on 1 July 2025.

If you are employed, what this will mean depends on the terms of your employment agreement. If your employment agreement states you are paid on a ‘total remuneration’ basis (base plus SG and any other allowances), then your take home pay might be reduced by 0.5%. That is, a greater percentage of your total remuneration will be directed to your superannuation fund. For those paid a rate plus superannuation, then your take home pay will remain the same, but your superannuation balance will benefit from the increase. If you are used to annual increases, the 0.5% increase might simply be absorbed into your remuneration review.

30% Tax on Super earnings for balances above $3m

The Government is pushing ahead with the proposed additional 15% tax on superannuation fund earnings for those with a total superannuation balance (TSB) above $3m. The legislation enabling the new tax (Division 296) is scheduled to commence from 1 July 2025.

If you are likely to be impacted by the tax, it is very important that the valuation of your superannuation assets is correct.

The Division 296 tax will apply for the first time to the growth in earnings (realised earnings from the sale of assets and unrealised earnings from the growth in the value of assets) between 1 July 2025 and 30 June 2026, for the portion above $3m.

The ATO will perform the calculation for the tax on earnings. TSBs in excess of the $3 million cap will be tested for the first time on 30 June 2026 with the first notice of assessment expected to be issued in the 2026-27 financial year.

Individuals will have the choice of paying the tax personally or from their superannuation fund. Those with multiple accounts can nominate which fund will pay the tax.

From fund perspective, reporting will form part of the current year-end tax return process.

Interests in defined benefit schemes will be appropriately valued and will have earnings taxed under this measure in a similar way to other interests.

If your superannuation balance is close to or above the $3m cap, it is important to seek advice on the best possible options for you.

What’s Not Changing

General transfer balance cap

The general rate for the transfer balance cap (TBC), that limits how much money you can transfer into a tax-free retirement account, will remain at $1.9 million for 2024-25. The TBC is indexed by the December consumer price index (CPI) each year.

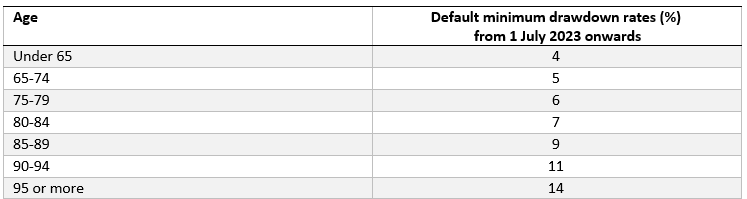

Minimum pension drawdown

The minimum pension drawdown, the amount you must draw from your pension each year, also remains the same:

Areas of ATO concern

Warning on sloppy valuations

The ATO has issued a warning to SMSF trustees about sloppy valuation practices. ATO data analysis has revealed that over 16,500 SMSFs have reported assets as having the same value for three consecutive years. Where asset values are consistently reported at the same value, it’s likely your SMSF will be flagged for closer scrutiny by the ATO.

The value of assets in your SMSF impacts on member balances and by default, can impact the amount you can contribute, your ability to segregate assets for exempt current pension income, the work test exemption, and access to catch-up concessional contributions.

If the asset is an in-house asset, for example a related unit trust, then an accurate valuation is essential to ensure the fund remains within the 5% in-house asset limit. If the value of in-house assets rises above 5% of total assets, the asset/s need to be sold to bring the limit back below 5%.

Valuation fundamentals

- Each year, the assets of your SMSF must be valued at ‘market value’ and evidence provided to your auditor.

- If your SMSF holds collectible and personal use assets like artwork, jewellery, motor vehicles etc., a valuation must be performed by a qualified independent valuer on disposal to a related party.

- The ATO require trustees to value assets based on “objective and supportable data.”

- Commercial and residential real estate does not need to be valued by an independent valuer but an independent valuer should be considered where there have been significant changes to the property or the market, the property represents a significant proportion of the fund’s value, or it is unique or difficult to value.

- If the trustees are completing the valuation themselves, ensure that you document the valuation date and the characteristics that contribute to the valuation (i.e., a 10 year old brick four bedroom property on 640m2 of land in what suburb and any features that make it more or less attractive to a buyer, for example proximity to transport). And, the trustees should access more than one source of credible comparative sales data either on similar properties in the same suburb that have sold recently or from a property data service. Do not use the generic values on online sales sites.

- For commercial property, net income yields are required to support the valuation. Where the tenants are related parties, for example your business leases a commercial property owned by your SMSF, you will need evidence that a comparative commercial rent is being paid and the rent is keeping pace with the market.

- For unlisted companies and unit trusts, the financials alone are not enough to support a valuation. Generally, the starting point is the value of the assets in the entity and/or the consideration paid for the shares/units. For widely held shares or units, this is the entry and exit price. Where property is the only asset, then the valuation principles for valuing real property are likely to apply.

Working with related parties

The ATO is actively reviewing arrangements between SMSFs and related parties, particularly where there are loans between the SMSF and a related party, property developments led by related parties that the SMSF has invested in, and distributions and entitlements from trusts controlled by related parties.

There are two problem areas the ATO is looking for; where structuring has the effect of minimising tax that would ordinarily be paid by an individual, and where there is little or no return to the SMSF for its investments, particularly where those investments are in entities controlled by members or other related parties.

Loans from related parties

Where the SMSF receives a loan from a related party under a limited resource borrowing arrangement (LRBA), the LRBA must be at market interest rates and repaid monthly. The ATO publish ‘safe harbour’ rates on their website each year. For 2024-25, the interest rate for real property is 9.35% and 11.35% for listed shares or units (8.85% and 10.85% respectively for 2023-24). Anything above or below this rate is likely to come under scrutiny from your auditor and the ATO. If trustees are unable to demonstrate the loan is on arm’s length terms, the non-arm’s length rules might apply (see Payments to related parties below).

Trust distributions and entitlements

The ATO is concerned about arrangements where an SMSF receives income or assets from a trust, particularly where:

- The trust has not paid the fund their entitlement to distributions for a number of years. The longer the amount remains outstanding, the more likely it will be considered a loan. If the distribution is considered a loan, this is likely to be problematic, particularly if the trust is an ungeared unit trust (SIS Regulation 13.22C).

- The ATO expects that the SMSF and all unit holders are treated consistently. This means that the SMSF should receive a fixed entitlement in line with their ownership interest in the trust. If the payment is more than expected, there is a risk that non-arm’s length income rules will apply to the distribution received by the SMSF. Within the trust, any dealings with related parties should also be on arm’s length terms to avoid non-arm’s length expense rules applying to the trust distribution.

Property developments

The ATO is reviewing arrangements involving closely held groups (which include an SMSF) and non-arm’s length dealings between group members. While the SMSF itself might not be involved in non-arm’s length dealings between related parties, if the other parties are not operating at arm’s length, this might be enough to breach the rules.

Where an SMSF is invested in a property development, the ATO expect to see returns. Investments in related party property developments where the returns are low will be scrutinised closely to ensure that the SMSF’s money is not being directed into the hands of members or related parties. The investment needs to make sense for the SMSF and have an expectation of viable returns relative to what the SMSF could achieve elsewhere.

Payments to related parties

Where payments are made by the SMSF to related parties (directly or to a related entity), it’s important to be aware of the rules. The non-arm’s length income (NALI) rules prevent superannuation trustees artificially increasing the balance of the fund using preferential arrangements with related parties. Currently, where expenses are not at arm’s length and below market rates, all income derived by the fund could be deemed to be NALI and taxed at the top marginal tax rate.

A trustee can only be paid by the SMSF for non-trustee duties if:

- The trustee provides the services to the general public as part of a business, and

- the trustee holds any relevant licenses and qualifications for the work.

Fund Housekeeping

SMSF Compliance Status removed if annual returns are late

If your SMSF’s annual return is more than two weeks overdue and you have not requested a deferral, the ATO will move your fund’s status on Super Fund Lookup from ‘Complying’ to ‘Regulation details removed’. The result is that your fund may not be able to accept contributions from employers or rollovers from APRA regulated funds.

If you are having trouble paying your tax liability, please let us know as soon as possible so we can negotiate a deferral or payment plan with the ATO on your behalf.

Contributions must be received by 30 June

To claim a tax deduction for super contributions (as an employer or as an individual), the payment needs to be received by the fund no later than 30 June. Merely incurring a liability is not enough. To claim a tax deduction for a personal contribution you need to lodge a notice of intent with the SMSF, advise the amount you intend to claim as a deduction, receive the confirmation from the fund of the tax deductibility of the contribution, and physically make the contribution.

Review and Rectify any outstanding compliance Issues

If your auditor has highlighted any breaches or issues in previous year fund audits, you should review and rectify these issues by 30 June.

Review the Fund’s Investment Strategy

Trustees are required to ‘regularly review’ the fund’s investment strategy. We recommend that trustees review the strategy, and document the review, at least annually or when the circumstances of the fund change.

Review Insurance inside your SMSF

SMSF trustees need to consider the need for insurance cover for the fund members when formulating and reviewing the fund’s investment strategy.

SMSFs are only able to offer or take out new insurance cover where the definitions are consistent with the death, terminal illness, permanent incapacity and temporary incapacity conditions of release under the Superannuation Industry Supervision Act.

It’s important that you review insurance inside your SMSF, not just for compliance with the law, but also effectiveness. An important issue to consider is how any insurance inside your fund should be structured; that is, from where the premiums are paid from the fund and what account any policy proceeds will be paid to inside the fund.

Correctly structuring insurance inside your fund can be complex. We recommend that SMSF Trustees seek the advice of their financial adviser to achieve the most tax effective outcomes for insurance proceeds, especially for ageing or unwell members.

Contributions you didn’t know you made

Trustees are often surprised by what is considered to be a contribution. Beyond money, these can include personally paying fund expenses, obtaining goods and services for less than market value, and some discretionary trust distributions. For example:

- In-specie transfer – If an asset is transferred or acquired from a related party for less than fair market value, the difference may be treated as a contribution.

- Capital improvements – Capital improvements to existing fund assets for no consideration or less than arm’s length consideration may be treated as a contribution.

- Debt forgiveness – A contribution is made if a loan, entered into by the fund is forgiven by the lender (related party). The contribution is made when the deed of release is executed that then relieves the fund from the obligation of repaying the debt.

- Guarantor arrangements – A contribution occurs if a guarantor to a debt of the fund (trustees in their own right) satisfies a loan obligation of the fund and then forgoes the right of redemption against the fund (trustees) itself.

What We Need From You

This is a general list of what we need to complete your fund’s tax and accounting requirements.

If you use software with data feeds, please ensure you adapt this section to remove items you do not need from the client such as bank statements, and some investment information.

- Bank statements (including any new accounts including term deposits) from 1 July 2023 to 30 June 2024.

- Contributions:

- A breakdown by member of the types of contributions received by the fund.

- Pensions:

- Documentation supporting any pensions commenced during the 2023-24 financial year.

- Investments:

- Portfolio valuation as at 30 June 2024 and transaction history reports (if applicable)

- All documentation from your portfolio or wrap provider including year end tax statements

- All dividend & tax statements

- Buy & sell contracts for shares sold or purchased

- Any other documentation received during the year that relates to takeovers, restructures, bonus shares, consolidations etc., for shares held by the fund. Usually these documents advise you to retain them for taxation purposes

- Any other document relating to an investment held within the fund which has not been covered above

- Property:

- Agent statements (either monthly or annual) if using an agent to manage property, otherwise, all invoices and rent receipts for the year ending 30 June 2024

- A copy of the current lease/rental agreement (if not already provided)

- Documents for property bought or sold, including the date you entered the contract and the date the asset was first used or installed ready for use

- Rental appraisal & market valuation from an agent (if you are using one to manage your property)

- Invoices for expenses paid

- Rollovers:

- Copy of any Rollover Benefits Statements for money rolled into the fund during the period 1 July 2023 to 30 June 2024

- Insurance:

- Copy of life insurance policy annual renewal documentation form (the ownership of the policy should always be in the name of the superannuation fund)

- Copy of documentation relating to any new insurance policies from 1 July 2023.

- Other:

- If you have transactions in your fund that do not fall into the above categories, please ensure that you provide us with full details